Unlock the DST Advantage: Turn Tax Headaches into Hands-Free Wealth — A Deep Dive for Indianapolis Investors

By Cara Conde | Indianapolis Luxury Real Estate Broker & Investor • April 2026

Imagine selling a well-appreciated rental property or commercial asset in Carmel, Geist, or on the north side and suddenly facing a six-figure capital gains tax bill — plus depreciation recapture. You want to defer every dollar possible while generating truly passive income that supports your lifestyle and funds the next iconic off-market estate in Zionsville or Meridian-Kessler.

A Delaware Statutory Trust (DST) has become one of the most powerful tools for sophisticated 1031 exchangers. It allows you to exchange into fractional ownership of institutional-grade, professionally managed real estate while staying fully tax-deferred.

With over 20 years as an Indianapolis Realtor® and Broker (licensed since 2002), and a background as an investor who built a multimillion-dollar personal portfolio, I’ve guided high-net-worth clients through both luxury residential purchases and advanced wealth-preservation strategies. This deep dive will give you the detailed knowledge you need to evaluate DSTs confidently in 2026.

Ready for personalized guidance on whether a DST fits your 1031 timeline or overall strategy?

Call or text me directly at (317) 999-9888 — available seven days a week.

What Exactly Is a Delaware Statutory Trust (DST)?

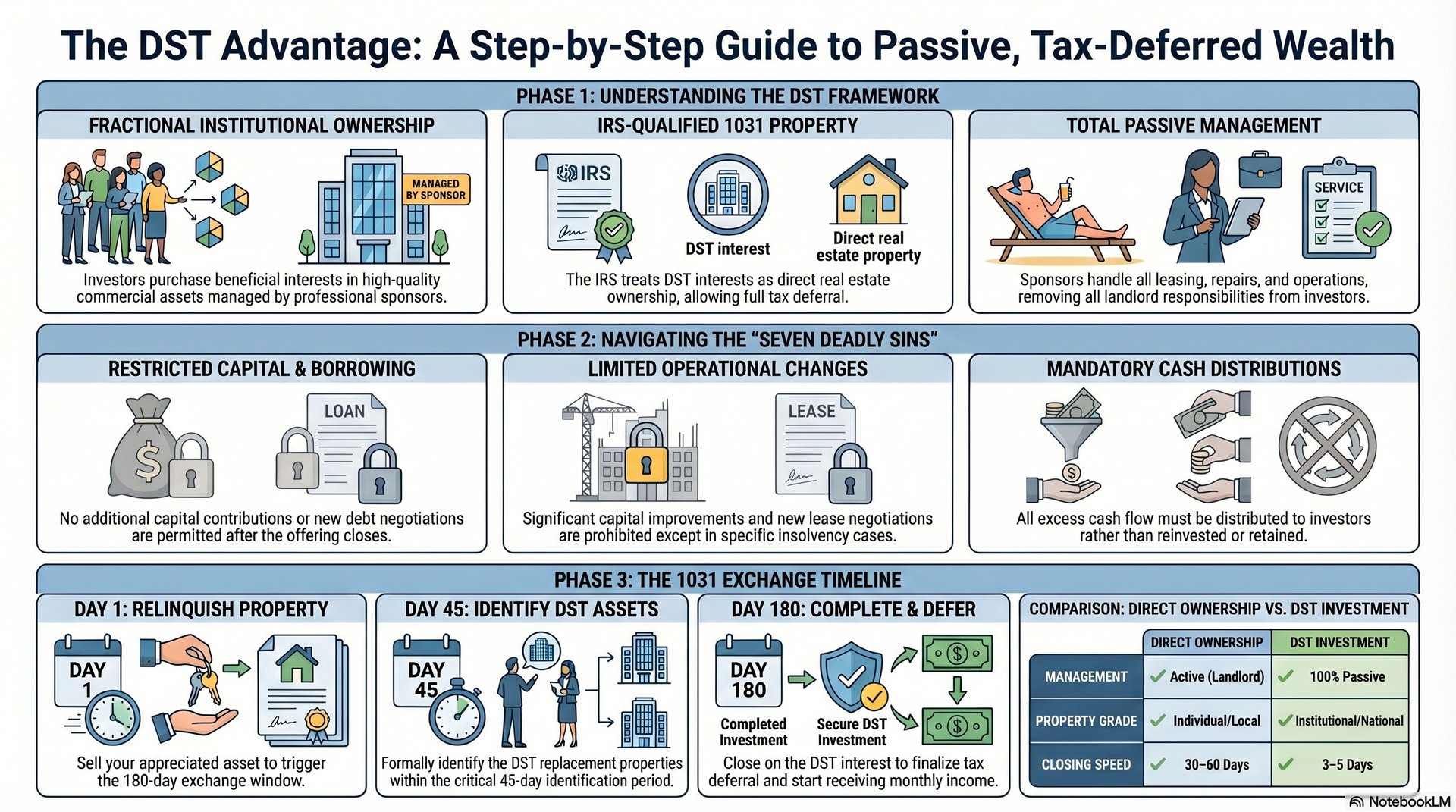

A DST is a legal entity formed under the Delaware Statutory Trust Act of 1988. It is structured as a grantor trust that holds title to one or more income-producing commercial real estate assets. Instead of owning the property directly, investors purchase beneficial interests — essentially fractional, undivided ownership shares in the trust.

The sponsor (a professional real estate firm) acquires the property, arranges financing, and handles all day-to-day management, leasing, and operations. Investors remain completely passive. For federal income tax purposes, the IRS treats ownership of a properly structured DST beneficial interest as direct ownership of real estate, which is why DSTs qualify for 1031 exchanges.

In 2026, most DST offerings focus on stabilized, institutional-quality assets with conservative leverage.

The History and Legal Evolution of DSTs

DSTs evolved from older common-law business trusts but gained modern clarity and flexibility with Delaware’s 1988 Statutory Trust Act. The pivotal moment arrived in 2004 when the IRS issued Revenue Ruling 2004-86, confirming that beneficial interests in a DST can qualify as “like-kind” replacement property in a 1031 exchange — provided the trust adheres to strict guidelines (commonly called the “seven deadly sins”).

Since then, DSTs have grown significantly in popularity, especially among time-constrained investors seeking diversification and passivity. In 2026, after a period of higher interest rates and pricing resets, DST sponsors are emphasizing lower-leverage structures and resilient cash-flow sectors.

The Seven Deadly Sins — IRS Rules That Protect (and Limit) DSTs

To maintain “like-kind” status and avoid being classified as an active business trust, DSTs must follow seven key restrictions from Revenue Ruling 2004-86. These rules are what make DSTs safe for 1031 treatment but also limit flexibility:

- No additional capital contributions after the offering closes. This prevents dilution of existing investors.

- No new borrowing or renegotiation of existing loans (with narrow exceptions for bankruptcy/insolvency).

- No material modifications to leases or entering new leases (except in cases of tenant insolvency).

- No significant capital improvements or expenditures beyond ordinary maintenance.

- No reinvestment of sale or refinance proceeds by the trustee.

- Excess cash must generally be distributed to investors rather than retained or reinvested.

- No operations that would classify the DST as a “business trust.”

These restrictions favor stabilized assets with strong, long-term tenants (e.g., net-lease or institutional multifamily), which aligns well with defensive strategies in 2026.

How DSTs Work in a 1031 Exchange — Step-by-Step

The process follows standard 1031 timelines: 45 days to identify replacement property and 180 days to complete the exchange. DSTs often close quickly (sometimes in just a few days after your relinquished property sells), which reduces timing pressure. You can combine multiple DSTs for better diversification while meeting debt and equity requirements.

Investors receive monthly or quarterly cash distributions and pass-through depreciation. Minimum investments typically start around $100,000–$500,000 for accredited investors. When the sponsor eventually sells or refinances the underlying asset (often after 5–10+ years), you can potentially 1031 out into another property.

Major Benefits of DST Investing

- Full deferral of capital gains and depreciation recapture taxes.

- Complete passivity — no tenant calls, repairs, or management responsibilities.

- Access to large, institutional-grade properties (multifamily, industrial, net-lease medical/retail, self-storage, data centers) that most individuals could never purchase alone.

- Instant geographic and property-type diversification.

- Steady income streams and depreciation benefits in a lower-leverage 2026 environment.

- Estate planning advantages, including potential step-up in basis.

Potential Risks and Drawbacks — With Mitigation Strategies

DSTs are illiquid with long hold periods and limited secondary markets. The seven deadly sins restrict sponsor actions, sponsor performance risk exists, and fees (acquisition, asset management, disposition) add up. Market, interest-rate, and property-specific risks also apply.

Mitigation in 2026: Choose sponsors with strong track records, focus on lower-leverage offerings in resilient sectors (industrial, net-lease), diversify across several DSTs, and work with experienced advisors. Many clients pair DSTs with local Indianapolis holdings for balance.

DSTs vs. Other Real Estate Investment Options

DSTs often outperform direct ownership or Tenant-in-Common (TIC) structures for busy investors needing speed and passivity. They differ from public REITs by offering direct real estate tax treatment and depreciation. Private syndications may offer more control but come with higher operational involvement.

The Indianapolis Angle: Why Local Luxury Investors Use DSTs in 2026

Indianapolis benefits from strong logistics, industrial growth, and multifamily demand. However, many high-net-worth clients wisely diversify nationally through DSTs to reduce concentration risk. The resulting passive cash flow can support purchases of exclusive off-market estates in Carmel, Zionsville, Geist, or Meridian-Kessler — exactly the white-glove service I specialize in.

How to Evaluate and Invest in a DST — 2026 Practical Checklist

Key factors: Sponsor experience and track record, property fundamentals and location quality, debt/leverage levels (favor lower in 2026), projected cash flow and internal rate of return, exit strategy, and fee transparency. Red flags include high leverage, unproven sponsors, or overly optimistic projections.

Assemble a team: Qualified Intermediary, tax advisor, and a trusted local advisor who understands both DSTs and the Indianapolis luxury market.

People Also Ask About Delaware Statutory Trusts

Are DSTs eligible for 1031 exchanges?

Yes — when properly structured under Revenue Ruling 2004-86 and the seven deadly sins are observed.

What property types are common in 2026 DST offerings?

Stabilized multifamily, industrial/warehouse, net-lease retail and medical offices, self-storage, and data centers — many with conservative leverage and strong tenants.

Are DSTs only for accredited investors?

Yes. Offerings are typically restricted to accredited investors under SEC rules.

How liquid are DST investments?

Generally illiquid with 5–10+ year hold periods and limited secondary markets, though some sponsors offer redemption features later in the hold.

Ready to Explore DSTs for Your Indianapolis Wealth Strategy?

Delaware Statutory Trusts offer a sophisticated, tax-efficient way to defer gains, generate passive income, and access institutional real estate — all while keeping your focus on the extraordinary Indianapolis lifestyle you’ve built.

Call or text me today at (317) 999-9888 for a confidential, no-obligation conversation. Whether you’re in the middle of a 1031 or planning ahead, I’m here seven days a week to help integrate DSTs into your broader goals.